Executive Summary

Your credit score doesn’t have to be a mystery that only updates once a month. What if your finance app could predict the exact impact of every spending decision before you make it? What if it could guide you toward better credit health through simple, daily conversations like having a financial advisor in your pocket?

AI-powered consumer finance apps are making this transformation possible. By combining conversational banking, predictive analytics, and real-time behavioral insights, these apps turn financial management from a dreaded chore into an engaging daily habit. The result? Users improve their credit scores faster while financial institutions see dramatically higher engagement and retention.

At Matellio, we specialize in building custom AI and GenAI solutions that help financial services companies create these transformative consumer finance experiences turning complex financial wellness into something accessible, engaging, and genuinely effective.

Introduction: The Credit Health Puzzle That Traditional Apps Can’t Solve

Picture this: Sarah checks her credit score on Monday. It was 640, not terrible, but not great. She knows she should improve it, but the traditional advice feels overwhelming: “Pay down your balances. Don’t miss payments. Keep credit utilization below 30%.” She understands the rules, but she doesn’t know where to start or what specific actions will move the needle fastest.

By Friday, she’s forgotten about it entirely.

This is the paradox of traditional consumer finance apps. They show you the problem but don’t help you solve it. They display your credit score but offer no personalized roadmap to improve it. They notify you about transactions but don’t explain how each decision affects your financial health.

The disconnect is costing everyone. Consumers struggle with credit health while financial institutions watch engagement rates plummet. McKinsey research indicates that personalized financial advice can result in a 20% increase in customer satisfaction [1], yet most apps still deliver generic, one-size-fits-all recommendations that users ignore.

This is where AI changes everything.

Modern AI-powered consumer finance apps don’t just track your money; they transform how you interact with it. Through conversational banking, predictive nudges, and behavioral analytics, these apps create an entirely new category of financial wellness tools. They turn passive credit monitoring into active credit improvement, and they make financial engagement feel natural rather than forced.

Why Traditional Consumer Finance Apps Fail to Drive Real Change

Before exploring what makes AI-powered apps different, let’s understand why conventional approaches fall short.

The Information Overload Problem

Traditional finance apps dump information on users without context. Your credit utilization is 45%—but is that actually hurting you? You spent $230 at restaurants this month—but is that above or below what you can afford given your specific financial goals?

When users can’t connect data to actionable insights, they disengage. Information without guidance creates confusion, not confidence.

The One-Size-Fits-All Trap

Most apps offer the same advice to everyone: create a budget, save more, pay down debt. But your financial situation isn’t generic. You might be recovering from medical debt while someone else is optimizing their credit mix for a mortgage. Cookie-cutter recommendations don’t address your specific circumstances, so they don’t drive behavior change.

The Engagement Gap

Financial health requires consistent daily actions, but most finance apps treat engagement like a monthly check-in. You log in, look at your accounts, maybe feel anxious, then disappear for weeks. This sporadic engagement pattern can’t create the behavioral habits necessary for meaningful financial improvement.

The Trust Deficit

Many users don’t trust that finance apps have their best interests at heart. Are credit card recommendations actually good for you, or just profitable for the app? Without transparency and genuine personalization, skepticism prevents users from following advice even when it’s sound.

These challenges explain why, despite dozens of personal finance apps in app stores, most consumers still struggle with credit health and financial wellness. The solution isn’t more features; it’s fundamentally rethinking how technology supports financial behavior change.

The AI Advantage: How Intelligent Systems Transform Consumer Finance

AI doesn’t just automate traditional finance app features; it enables entirely new capabilities that weren’t possible before. Here’s how:

Conversational Banking Makes Finance Feel Human

Nobody wants to navigate complex menus when they have a simple question. AI-powered chatbots and virtual assistants bring natural conversation to financial management.

Statistics indicate that up to 60% of customer interactions can be seamlessly handled by digital assistants [2], freeing users from navigating complicated interfaces. Instead of searching through tabs to find “How much can I spend on groceries this week?”, you simply ask and get an instant, personalized answer based on your income, bills, goals, and spending patterns.

These conversational interfaces adapt to your communication style, remember context across sessions, and proactively reach out when they spot opportunities or risks. It’s the difference between interrogating a database and chatting with a knowledgeable friend.

Predictive Analytics Shows the Future Impact of Today’s Decisions

The most powerful aspect of AI in consumer finance is prediction. Traditional apps tell you what happened. AI apps tell you what will happen if you make certain choices.

Considering that streaming service subscription? Your AI assistant can instantly calculate how it affects your monthly budget, your ability to pay down credit card debt, and ultimately your projected credit score three months from now. This predictive power transforms decision-making from guesswork into informed choice.

Financial institutions using AI in credit assessment and customer assistance can improve customer financial health while managing risk more effectively [3]. When users can see the exact impact of their choices, they make better decisions which improve both their credit health and the institution’s portfolio quality.

Behavioral Analytics Understands Your Unique Financial Personality

AI systems analyze thousands of data points about your financial behavior to build a complete picture of your financial personality. They identify patterns you might not notice yourself: You consistently overspend on Fridays. Your savings rate drops in October. You’re more likely to make impulse purchases when stressed.

The behavioral analytics market is experiencing explosive growth; Fortune Business Insights valued it at $801.8 million in 2023 and predicts it will reach $11.5 billion by 2032 [4]. This growth reflects the immense value of understanding behavioral patterns.

Armed with these insights, AI can deliver perfectly timed interventions. A gentle reminder before your typical Friday splurge. A celebratory message when you break a negative pattern. Encouragement precisely when you need motivation to stick with your debt payoff plan.

Real-Time Credit Health Optimization

Perhaps most importantly, AI systems can continuously optimize your path to better credit health. They monitor your credit utilization, payment history, credit mix, and other factors, then provide specific, prioritized recommendations based on what will improve your score most efficiently. Should you pay down Credit Card A or Credit Card B first? Should you request a credit limit increase or focus on reducing balances? AI evaluates all variables simultaneously and guides you toward the highest-impact actions, turning credit improvement from guesswork into a clear strategy.

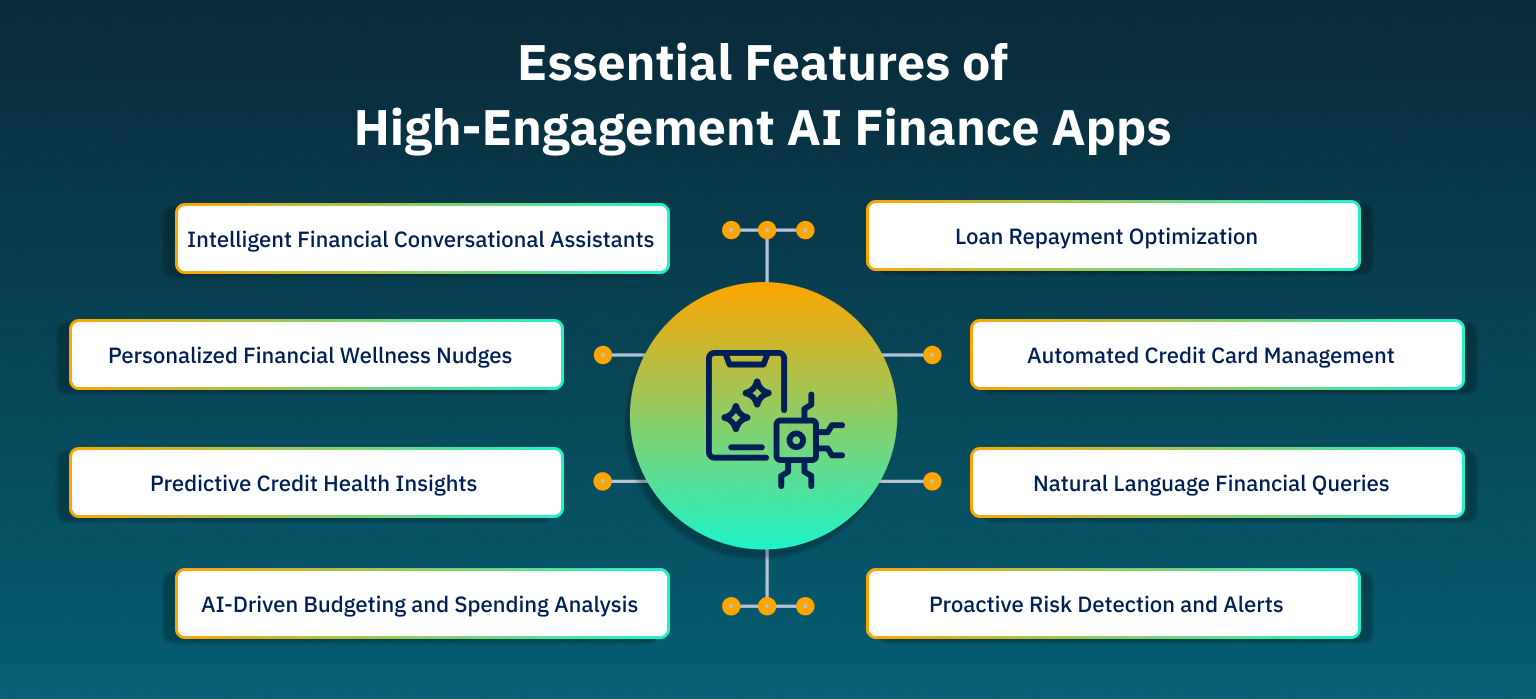

Essential Features of High-Engagement AI Finance Apps

Building an AI-powered consumer finance app that actually changes behavior requires more than throwing chatbots at existing features. Here are the must-have capabilities:

1. Intelligent Financial Conversational Assistants

Your app needs a conversational AI that goes beyond scripted responses. The best systems use large language models (LLMs) to understand natural language queries, maintain context across conversations, and provide genuinely helpful answers.

These assistants should handle everything from simple balance inquiries to complex financial planning questions. They should proactively reach out with insights: “I noticed you’re close to your spending limit for dining out this month. Would you like to adjust your budget or extend it slightly?”

2. Personalized Financial Wellness Nudges

Nudges are gentle prompts that guide users toward better financial decisions without being intrusive. AI makes nudges truly personal by timing them perfectly and customizing them to individual circumstances.

Examples include:

- “Your credit utilization just dropped below 30%, great job! This should positively impact your score next month.”

- “You have $150 available in your budget. Want to put $50 toward your emergency fund goal?”

- “Payday is tomorrow. Setting up that automated savings transfer now will help you reach your goal two months faster.”

The key is relevance and timing. Generic weekly reminders get ignored. Perfectly timed, personalized nudges drive action

3. Predictive Credit Health Insights

Users need to understand the “why” and “what next” of their credit health. AI-powered apps should explain:

- Which factors are currently helping or hurting their score

- What specific actions will have the biggest positive impact

- How long it will take to reach their target score if they follow recommendations

- The predicted impact of major decisions (opening a new card, paying off a loan, etc.)

This predictive capability transforms credit scores from confusing numbers into actionable roadmaps.

4. AI-Driven Budgeting and Spending Analysis

AI should automatically categorize transactions, identify spending patterns, and create budgets that adapt to your life. When income or expenses change, the system adjusts recommendations accordingly.

More importantly, AI should catch concerning patterns early: “Your average daily spending is 30% higher than last month. Would you like to review your transactions together?”

5. Loan Repayment Optimization

For users managing debt, AI can create optimal repayment strategies based on interest rates, balances, minimum payments, and cash flow. These systems calculate the fastest path to debt freedom while maintaining healthy credit utilization.

They should also provide motivational tracking: “You’ve paid off 23% of your total debt! At this pace, you’ll be debt-free in 18 months.”

6. Automated Credit Card Management

AI can monitor credit card utilization across all accounts and provide specific guidance: “Your Discover card is at 42% utilization. Paying an extra $150 before your statement closes would drop you below 30% and potentially improve your score.”

Some advanced systems can even automate balance optimization, suggesting strategic payments across multiple cards to minimize total interest while maximizing credit score impact.

7. Natural Language Financial Queries

Users should ask financial questions in plain English and get clear, personalized answers:

- “Can I afford to buy a $800 laptop this month?”

- “When will I have enough saved for a down payment?”

- “What’s the fastest way to improve my credit score?”

The AI processes these queries in context with the user’s complete financial picture and provides actionable guidance.

8. Proactive Risk Detection and Alerts

AI systems can identify potential problems before they become serious. Unusual spending patterns might indicate fraud. A consistently low balance combined with upcoming bills might predict an overdraft. A pattern of late payments suggests the user needs help with payment automation.

These early warnings, delivered with solutions rather than just problems, help users avoid financial setbacks.

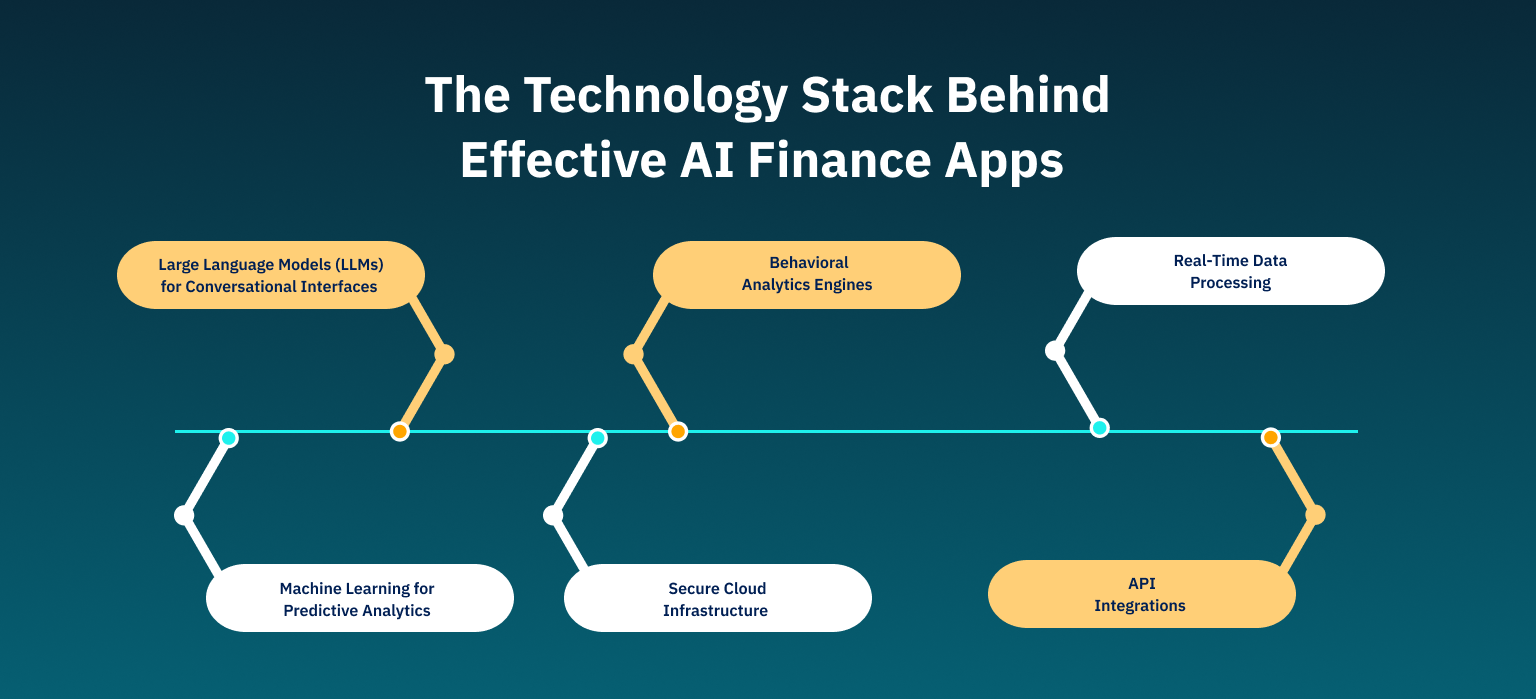

The Technology Stack Behind Effective AI Finance Apps

Creating these capabilities requires the right technical foundation. Here’s what works:

Large Language Models (LLMs) for Conversational Interfaces

Modern conversational banking relies on LLMs that understand natural language, maintain context, and generate human-like responses. These models power the chatbots and virtual assistants that make financial guidance feel personal and accessible.

The key is fine-tuning these models on financial terminology and compliance requirements. Generic chatbots make mistakes with financial advice; specialized financial LLMs provide accurate, helpful guidance.

Machine Learning for Predictive Analytics

ML algorithms analyze historical financial data to predict future outcomes. They identify which variables most strongly predict credit score changes, default risk, spending patterns, and financial stress.

These predictions enable proactive intervention: preventing problems before they occur rather than reacting after damage is done.

Behavioral Analytics Engines

Specialized analytics platforms track user interactions, identify patterns, and segment users based on financial behavior. This enables personalization at a scale; every user gets guidance tailored to their specific behavioral profile.

Secure Cloud Infrastructure

Financial applications require robust security, regulatory compliance, and scalability. Cloud platforms provide the infrastructure to handle sensitive financial data while meeting HIPAA-equivalent standards for financial services.

Real-Time Data Processing

Effective nudges and predictions require real-time data processing. Transaction data must flow instantly from banks and credit bureaus into analytical systems that generate insights and trigger interventions.

API Integrations

Consumer finance apps need to integrate with banking systems, credit bureaus, payment processors, and third-party financial services. Robust API architecture enables these integrations while maintaining security and data privacy.

Compliance and Privacy: Building Trust Through Transparency

AI-powered finance apps handle extremely sensitive personal information. Building user trust requires going beyond minimum compliance to embrace privacy as a competitive advantage.

Regulatory Compliance Frameworks

Financial services apps must comply with regulations including:

- Fair Credit Reporting Act (FCRA): Governs how credit information is collected, shared, and used

- Gramm-Leach-Bliley Act (GLBA): Requires financial institutions to protect customer information

- State privacy laws: Including CCPA in California and similar laws in other states

AI systems must be designed with these regulations in mind from the start. Compliance can’t be an afterthought.

Responsible AI Lending Practices

When AI influences credit decisions or provides credit advice, it must avoid bias and discrimination. This requires:

- Regular algorithm audits for fairness across demographic groups

- Transparency about how AI makes recommendations

- Human oversight of significant financial decisions

- Clear explanation of factors influencing credit assessments

Data Security and Encryption

All financial data must be encrypted in transit and at rest. Access controls should follow the principle of least privilege. Regular security audits and penetration testing ensure vulnerabilities are identified and addressed.

User Transparency and Control

Users should understand:

- What data the app collects

- How AI uses their data to generate insights

- Who has access to their information

- How to delete their data or opt out of AI features

Transparency builds trust. Users who understand and approve of how their data is used become advocates rather than skeptics.

Real-world impact :What Success Looks Like

When Ai powered consumer finance apps are build correctly, they deliver measurable results for both users and financial institutions

The Matellio Approach: Custom AI Solutions for Financial Services

At Matellio, we’re build custom AI and GenAI software that transform how financial services companies serve their customers.

Our Expertise in Financial AI

We’ve built intelligent systems for clients across financial services, helping them leverage AI to create better customer experiences while managing risk and maintaining compliance. Our approach combines:

- Deep AI/GenAI Capabilities: From conversational AI powered by large language models to predictive analytics and behavioral modeling, we implement the latest AI technologies tailored to financial services requirements.

- Financial Services Experience: We understand the unique challenges of building financial applications which involves regulatory compliance, security requirements, integration complexity, and the need for accuracy and reliability.

- Custom Development Philosophy: Every financial institution has unique needs. We don’t offer one-size-fits-all solutions. Instead, we build custom platforms that address your specific business challenges and customer segments.

Proven Success in AI-Powered Platforms

We are trusted by leading Fortune 500 companies. Our work demonstrates our ability to build sophisticated AI systems that scales with enterprise growth.

End-to-End Development Partnership

When you work with Matellio, you get:

- Requirements analysis and strategic planning to define the optimal AI solution for your business goals

- Custom AI/ML model development tailored to your specific use cases and data

- Secure, scalable architecture that grows with your user base

- Compliance-first design that meets all financial services regulatory requirements

- Comprehensive testing and quality assurance ensuring reliability and accuracy

- Ongoing optimization and support to continuously improve AI performance

We follow agile development methodologies that keep you involved throughout the process, ensuring the final product matches your vision while exceeding your users’ expectations.

Building Your AI-Powered Consumer Finance App: A Strategic Roadmap

Ready to create an AI-powered consumer finance app? Here’s the strategic path forward:

Phase 1: Define Your Unique Value Proposition

What specific problem will your app solve better than alternatives? Maybe it’s credit health improvement for millennials. Perhaps it’s debt payoff optimization for healthcare workers. Or financial wellness for gig economy workers with irregular income.

Your AI capabilities should directly support this value proposition, not just exist as buzzwords.

Phase 2: Understand Your Users Deeply

Conduct user research to understand:

- Their current financial pain points

- How they currently manage credit health

- What prevents them from achieving financial goals

- What would motivate daily engagement with your app

This research informs everything from feature prioritization to conversational AI personality.

Phase 3: Design the Conversational Experience

Map out the key conversations your AI will have with users. How will it introduce itself? How will it deliver bad news? How will it celebrate wins? The conversational design creates the emotional connection that drives engagement.

Phase 4: Build Your AI Core

Develop the AI and ML systems that power your platform:

- Conversational AI for natural language interaction

- Predictive models for credit health forecasting

- Behavioral analytics for personalization

- Recommendation engines for financial guidance

This technical foundation must be built with accuracy, security, and compliance as non-negotiable requirements.

Phase 5: Integrate Financial Data Sources

Connect to banking systems, credit bureaus, and other data sources through secure APIs. Real-time data flow is essential for timely interventions and accurate predictions.

Phase 6: Launch, Learn, and Optimize

Start with an MVP focused on your core value proposition. Gather user feedback aggressively. Monitor which AI features drive engagement and which fall flat. Continuously optimize based on real usage data.

AI systems improve over time as they learn from more data. Your initial launch is just the beginning of an ongoing optimization process.

Conclusion: The Future of Financial Wellness is Conversational

The transformation happening in consumer finance isn’t about adding AI features to existing apps. It’s about fundamentally reimagining how technology supports financial wellness.

When finance apps can predict impacts, explain decisions, adapt to individual circumstances, and guide users through natural conversation; they stop being tools you occasionally check and become partners in your financial journey.

The financial institutions that embrace this transformation won’t just see better engagement metrics. They’ll build genuine loyalty by helping customers achieve real financial improvements. Users whose credit scores improve, whose debt decreases, whose emergency funds grow—these users become advocates who refer friends and stick around for life.

The technology to build these transformative apps exists today. What’s needed is the vision to move beyond transactional banking toward truly intelligent financial partnership and the technical expertise to build AI systems that are secure, compliant, and genuinely helpful.

Key Takeaways

- AI transforms consumer finance from passive monitoring to active improvement – Users get personalized guidance that actually changes behavior

- Conversational banking makes financial management accessible – Natural language interfaces remove barriers to engagement

- Predictive analytics empowers better decisions – Users see the future impact of choices before making them

- Behavioral insights enable perfect timing – AI delivers the right message at exactly the right moment

- Compliance and privacy build trust – Transparent, responsible AI creates competitive advantage

- Engagement drives credit health improvement – Daily interactions create the behavioral patterns necessary for lasting financial change

- Custom development matters – One-size-fits-all AI platforms can’t address your unique user needs and business model

FAQ’s

Yes, when they are designed well. AI powered personal finance apps can improve credit health by giving specific, personalized actions like which card to pay down and by how much, sending timely nudges that build consistent habits, and optimizing which steps will have the biggest impact on your score. The real value comes from genuine personalization and ongoing engagement, not just slapping an AI label on generic advice.

The best AI powered consumer finance apps keep people engaged by making money management feel simple, timely, and a bit rewarding. Core features include a conversational assistant so users can ask questions in plain language and get instant, personalized answers, proactive nudges that arrive at the right moment instead of generic reminders, predictive insights that show how today’s choices affect future outcomes, and clear visual progress tracking that celebrates small wins.

On top of that, light gamification such as streaks, milestones, and rewards makes good habits stick, while bite sized financial education appears in context when the user actually needs it. The common thread is that AI uses data to deliver interactions that feel relevant and helpful, not spammy or intrusive.

AI chatbots in personal finance apps can be highly accurate when well-designed, offering consistent, error-free advice based on complete financial data, rules, and regulations. However, poorly implemented chatbots can give incorrect advice, especially if trained on generic internet data. To ensure accuracy, they should be trained on financial services data, regularly audited, and supervised by humans for major decisions. Reputable apps include disclaimers and route complex questions to human advisors while using AI for routine guidance.

Yes, AI-driven spending analysis and budgeting nudges can significantly enhance financial wellness. Behavioral economics shows that small, well-timed nudges can greatly influence decisions, and AI makes these nudges personal and timely. McKinsey research shows personalized advice boosts customer satisfaction by 20%, leading to better financial outcomes [1]. AI systems detect spending patterns, time interventions, adapt to life changes, and provide accountability, making users feel like they have a financial coach who understands their needs and helps them stay on track.

AI apps optimize credit card repayment and loan management by analyzing factors like interest rates, credit score impact, and cash flow. They create personalized repayment strategies, balancing which debts to pay first, maintaining healthy credit utilization, and ensuring timely payments. AI also adapts strategies to user behavior, offering motivational reinforcement. For loans, it tracks due dates, identifies refinancing opportunities, and suggests ways to reduce interest costs or shorten terms.

Privacy concerns in AI-powered finance apps include data collection scope, potential sharing with third parties, lack of transparency in AI decision-making, security risks, and behavioral manipulation. Responsible apps address these by minimizing data collection, offering transparent privacy policies, giving users control over their data, ensuring regulatory compliance, and prioritizing security. Choose reputable apps that clearly explain their privacy practices and align their incentives with user success.

Whether users would trust an app predicting their financial behavior depends on factors like trust in the provider, transparency, control, track record, and privacy protections. Users are more likely to embrace AI-powered financial apps if they understand how the predictions work, maintain control over decisions, see privacy protections in place, and experience accurate results over time. The key for providers is to build trust through transparency, demonstrated success, and alignment with user financial goals.

References:

1. Tech-Azur. (2024). “The future of Fintech: navigating employee and customer experiences for 2024’s success.” Retrieved from https://tech-azur.com/blog/navigating-the-future-of-fintech-whats-next-in-2024

2.Instinctools. (2025). “Conversational AI In Banking: Real-World Use Cases and Challenges.” Retrieved from https://www.instinctools.com/blog/conversational-ai-in-banking/

3.McKinsey & Company. (2024). “The promise of gen AI for credit consumer services.” Retrieved from https://www.mckinsey.com/capabilities/risk-and-resilience/our-insights/the-promise-of-generative-ai-for-credit-customer-assistance

4. RiskSeal. (2025). “What Is Behavioral Analysis for Credit Scoring?” Retrieved from https://riskseal.io/glossary/behavioral-analysis