Executive Summary

Financial institutions are facing growing exposure to fraud as digital banking becomes more widespread and accessible. In 2023 alone, projected global losses from fraud scams and banking schemes exceeded $485.6 billion, an alarming indicator of the evolving threat landscape. [1] In the US alone, total losses from credit card/check fraud amounted to around $199.9 million in 2024, highlighting the scale of impact. [2]

Traditional rule-based systems are no longer sufficient to detect today’s sophisticated threats, such as synthetic identities, account takeovers, and coordinated money laundering operations.

Data analytics in banking and financial services is reshaping how banks approach risk management and regulatory compliance. With advanced machine learning models analyzing transactional behavior in real time, institutions can detect anomalies earlier and more accurately. This not only reduces fraud losses but also minimizes false positives, streamlines investigations, and improves customer experience.

By adopting AI-powered analytics, financial institutions shift from reacting to threats to proactively preventing them, building scalable, adaptive defenses that keep pace with both risk and regulatory demands.

I. Why Traditional Risk Management Can’t Keep Up With Modern

As fraud tactics become more sophisticated, financial institutions are facing increased exposure, not only to monetary loss but also to regulatory penalties, customer attrition, and operational disruption. Over half of US-based banks, fintechs, and credit unions report an increase in fraud in business accounts, with a quarter of them losing $1 million or more due to fraud. [3]

Legacy Risk Management Leaves Critical Gaps

Traditional risk infrastructures built on static rules, legacy systems, and historical transaction patterns are no longer sufficient. These systems often detect fraud after the damage is done, lacking the real-time agility needed to keep pace with modern attack vectors, such as synthetic identities, mule networks, and automated phishing schemes.

More critically, these outdated systems can compromise operational efficiency, delaying investigations, overwhelming teams with false positives, and creating friction in customer experiences.

AI-Driven Fraud Tactics Are Outpacing Legacy Defenses

Modern fraudsters exploit this gap, using AI and machine learning to bypass static defenses. Banks could pay an estimated $40 billion in fraud losses by 2027 [4] as advances in generative AI help cybercriminals create more convincing phishing schemes, deepfakes, and synthetic identities. Synthetic identities alone account for more than 80% of all identity fraud, slipping past conventional filters and creating long-term exposure. [5] This makes traditional fraud detection methods increasingly obsolete.

II. Modern Risk Management Begins with Real-Time Data Intelligence

Modern fraud prevention begins the moment a customer initiates an interaction. Real-time data analytics platforms in financial services continuously ingest and process high-velocity data streams across multiple dimensions: transaction metadata, user behavior, network traffic, and system events.

Technical Foundations

To handle this complexity, banks are deploying:

- Stream processing engines like Apache Kafka and Apache Flink to process events with sub-second latency.

- In-memory computing frameworks (e.g., Hazelcast, Redis) that power real-time scoring models by storing frequently used data and risk models in volatile memory for immediate access.

- Event-driven architectures that trigger custom workflows and alert the moment suspicious activity is detected.

- Device Fingerprinting: Unique hardware/software combinations are checked for consistency across sessions and channels.

- Behavioral Biometrics: Systems track how a user types, moves their mouse, or swipes on mobile devices, creating individualized behavioral baselines.

- Transactional Velocity and Frequency Analysis: Unusual patterns (like rapid transfers between new accounts) raise red flags in near-real time.

Seamless Integration Without Performance Trade-Offs

Modern systems use microservices-based APIs to integrate with core banking systems, payment gateways, and fraud orchestration layers. Risk scores, fraud flags, and audit logs are piped into SIEM tools and compliance dashboards without interrupting the transaction flow so that customers never experience added latency or friction.

III. How Machine Learning Raises the Bar for Fraud Detection

Machine learning algorithms revolutionize fraud detection in finance through their adaptive learning capabilities, which evolve in response to emerging threats. Unlike static, rule-based systems, these models continuously learn from new data, evolving to identify even the most sophisticated fraud patterns in real-time.

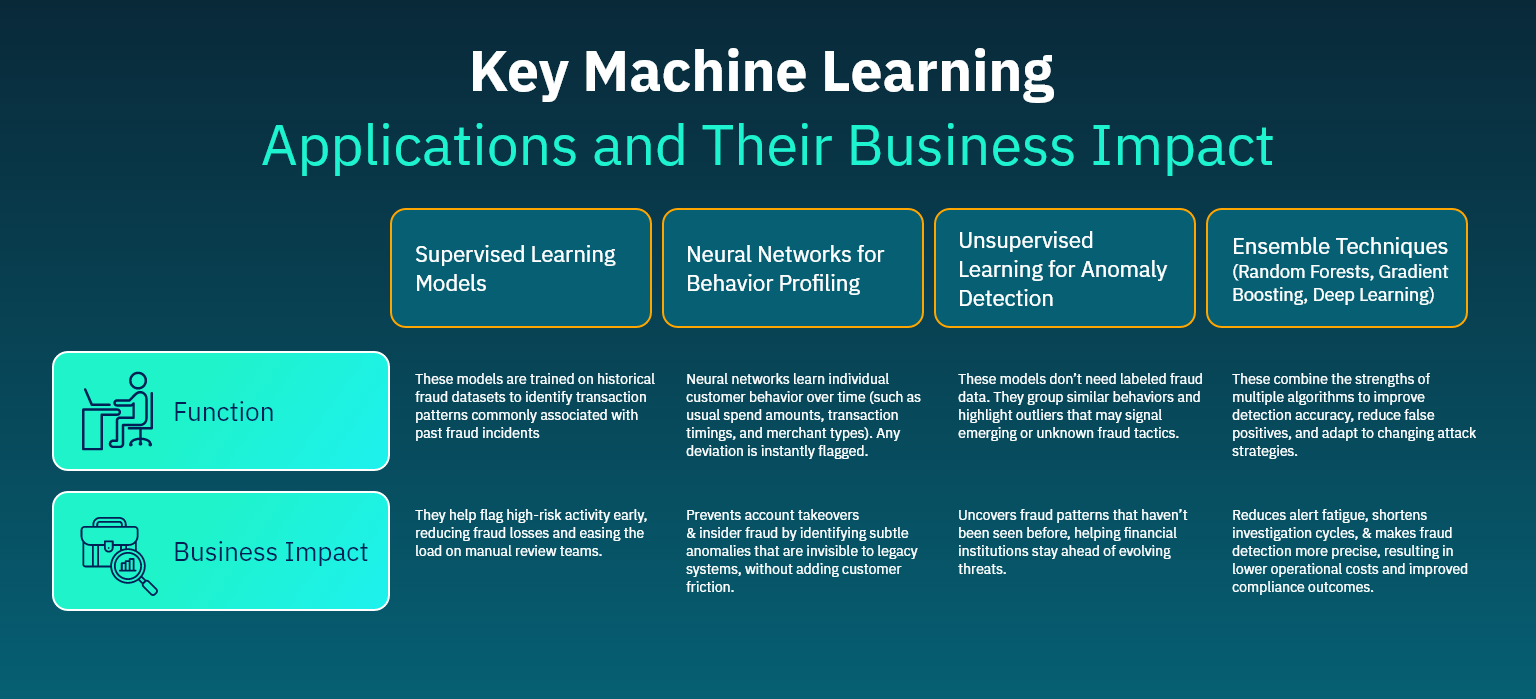

Key Machine Learning Applications and Their Business Impact

Machine learning in financial risk analytics is about preventing fraud before it hurts your bottom line. Here’s how specific models deliver measurable business value:

IV. Detecting Fraud Starts with Relationship Mapping and Network Intelligence

Risk analytics platforms map complex relationships between accounts, devices, locations, and individuals to identify coordinated fraud schemes spanning multiple customer profiles. These platforms analyze connection patterns, transaction flows, and behavioral similarities to detect organized criminal networks operating across institutions, flagging entire fraud rings rather than investigating individual accounts.

This capability is powered by a range of advanced techniques, including:

- Community detection algorithms that group related entities across multiple accounts, making it easier to spot coordinated fraud activity.

- Velocity monitoring to detect rapidly expanding networks that signal fraud proliferation, including bot-driven account creation and automated schemes.

- Suspicious cluster analysis that maps transaction flows to reveal organized money laundering operations undetectable by traditional .

This level of connected intelligence lays the foundation for proactive compliance automation in finance, where tracking relationships, behaviors, and risk patterns helps meet regulatory standards while reducing manual reviews.

V. Strengthening Compliance Automation in Finance with Integrated KYC/AML Intelligence

Routine checks alone are insufficient for regulatory compliance in banking within a multi-jurisdictional environment. It demands intelligent systems that can respond to policy changes and regulatory updates as they happen. With institutions spending over $30.9 million annually on compliance efforts , [6] it’s critical to build smarter processes that balance accuracy with cost control.

Integrating Analytics with KYC/AML Systems: An analytics platform that integrates seamlessly with existing KYC/AML systems while enhancing detection for complex money laundering schemes not only strengthens regulatory alignment but also helps control the escalating costs of compliance.

Automating Screening and Reducing False Positives: Modern compliance platforms use automated screening to compare customer data against global watchlists, sanctions databases, and politically exposed person registries. Machine learning filters out obvious false positives while prioritizing high-risk matches for review, improving both accuracy and speed.

Real-Time Risk Scoring and Alerts: Dynamic risk-scoring engines monitor behavior in real time, flag anomalies, generate alerts, and provide detailed evidence for compliance teams.

Extending Automation Beyond Transactions: Beyond transaction monitoring, automation also covers ongoing customer due diligence, periodic reviews, profile updates, and adverse media monitoring. This approach maintains consistent compliance while reducing manual oversight and operational strain.

VI. Case Study: How SEPS Used AI to Modernize Regulatory Oversight and Consumer Protection

SEPS, Ecuador’s financial regulatory authority, faced critical operational challenges due to fragmented claim management processes and manual compliance tracking.

The Challenge

Key issues included:

- Delayed claim resolution and case escalations due to manual workflows

- Limited visibility into market-level regulatory violations

- Inconsistent tracking of financial institution compliance

- Lack of real-time support for consumers

- Poor integration with identity verification systems

To address these inefficiencies and modernize financial consumer protection, SEPS needed a robust AI-powered platform to automate workflows, enhance regulatory agility, and improve transparency for both regulators and consumers.

The Solution

Matellio, in collaboration with Cambridge SupTech Lab and the World Bank, built a Financial Consumer Protection Suite tailored to SEPS’ needs. The platform integrated advanced analytics and intelligent automation across three core systems:

- Claims Management System (CMS): Automated intake, triaging, and tracking of consumer claims

- AI-Powered Chatbot: Delivered instant responses in Spanish, reduced human workload, and supported real-time escalations

- Data Analytics Dashboard: Provided SEPS with real-time regulatory insights into claim trends, institutional violations, and market behavior

- Civil Registry API Integration: Enabled secure identity validation to streamline compliance checks and fraud prevention

The Impact

The solution brought measurable improvements in compliance oversight and consumer service:

- 40% faster claim resolutions through process automation

- Thousands of inquiries handled autonomously via AI chatbot

- Enhanced supervisory decision-making with real-time regulatory insights

- Secure, API-driven identity verification improving compliance accuracy

- Elevated market transparency and consumer trust through intelligent automation

The SEPS case study shows how regulatory bodies, and by extension, financial institutions, can improve efficiency, transparency, and compliance using AI and real-time analytics. Businesses can replicate this by investing in modular, API-driven platforms that combine AI-powered automation, real-time dashboards, and secure identity validation to streamline compliance workflows and elevate customer support.

The key is to start with one high-friction area, then scale with intelligent components that integrate seamlessly.

VII. Building Scalable Risk Defenses with AI and Advanced Analytics

Traditional rule-based systems leave financial institutions exposed to modern fraud and compliance risks. Fraud detection in finance with data analytics changes that by enabling real-time, adaptive detection powered by machine learning, entity mapping, and automated workflows. This shift not only reduces false positives and improves threat response but also streamlines compliance, turning fragmented defenses into a cohesive, intelligent system.

Matellio empowers financial institutions with cutting-edge analytics designed for modern risk landscapes. From fraud detection to compliance automation, our solutions deliver agility, accuracy, and resilience, ensuring your risk management strategies evolve as fast as the threats you face.

Transform your risk management with real-time analytics.

Schedule a consultation today to minimize fraud losses and streamline compliance ahead of the next regulatory audit.

Ready to modernize your systems?

See how the right enterprise tech partner can accelerate your growth.

Key Takeaways

- Real-time processing capabilities are essential for modern fraud detection systems. Your institution must invest in streaming analytics platforms that analyze transactions as they occur rather than after completion to prevent fraudulent activities and maintain a competitive advantage.

- Machine learning algorithms significantly outperform rule-based systems in detecting sophisticated fraud schemes. These adaptive models learn from new fraud patterns while maintaining high accuracy rates across diverse attack vectors and emerging threats that traditional systems cannot identify.

- Network analysis reveals coordinated fraud schemes that escape individual account monitoring systems. Graph-based analytics identify relationships between entities that indicate organized criminal activity requiring immediate investigation and coordinated response efforts across multiple channels.

- Integration with existing KYC/AML systems creates comprehensive compliance frameworks for regulatory adherence. Your analytics platform must connect with regulatory systems to ensure continuous monitoring and automated reporting capabilities while maintaining comprehensive audit trails throughout all processes.

- Data governance frameworks are crucial for managing privacy and regulatory requirements. Proper governance ensures that the implementation of data analytics in banking and financial services complies with data protection regulations while maximizing analytical value and operational effectiveness across all business units.

FAQ’s

Banks establish robust data governance frameworks that protect customer data while supporting risk management analytics. These include role-based access, encryption, and audit trails to monitor data use. Techniques like anonymization, pseudonymization, differential privacy, and federated learning enable secure analysis without exposing sensitive customer information.

Modern cloud platforms offer advanced security and compliance features that often surpass traditional on-prem standards for financial institutions. With built-in controls for data residency, auditing, and industry-specific regulations, leading providers support regulatory compliance in the banking sector. By selecting the right vendors and ensuring proper oversight, banks can leverage cloud analytics while maintaining continuous compliance across all operations.

Data governance provides the framework that keeps analytics secure, compliant, and reliable. It sets clear ownership, access rules, and usage policies, ensuring data is accurate, well-managed, and trusted. This structure allows teams to innovate while maintaining control in financial analytics projects.

References:

[1] https://www.nasdaq.com/global-financial-crime-report

[2] https://www.ic3.gov/AnnualReport/Reports/2024_IC3Report.pdf

[3], [4] https://www.alloy.com/blog/2024-fraud-stats-for-banks-fintechs-and-credit-unions

[5] https://www.biometricupdate.com/202410/report-synthetic-identity-fraud-is-growing